Over the past year, many businesses that received Employee Retention Credit refunds have completed the audit cycle. While many examinations have resulted in no change, in a growing number of cases, the IRS has disallowed the Credit and assessed some or all of the refunded amount as additional tax. Businesses then repaid the assessed tax, along with interest that the IRS calculated on the underpayment. For many of these taxpayers, repayment probably seemed like the end of the matter. But a recent court decision interpreting tax-related deadlines during Federally declared disasters may create an unexpected refund opportunity for many of those businesses.

If the Court of Federal Claims’ interpretation of section 7508A(d) in Kwong v. United States ultimately proves correct, some taxpayers may have paid interest that should never have accrued in the first place. To be sure, in matters currently being evaluated by our firm, interest overpayments routinely reach tens of thousands of dollars and in some cases climb to more than $50,000 or more. We encourage businesses that made repayment of ERC to review their situation to see if they might be in a similar situation.

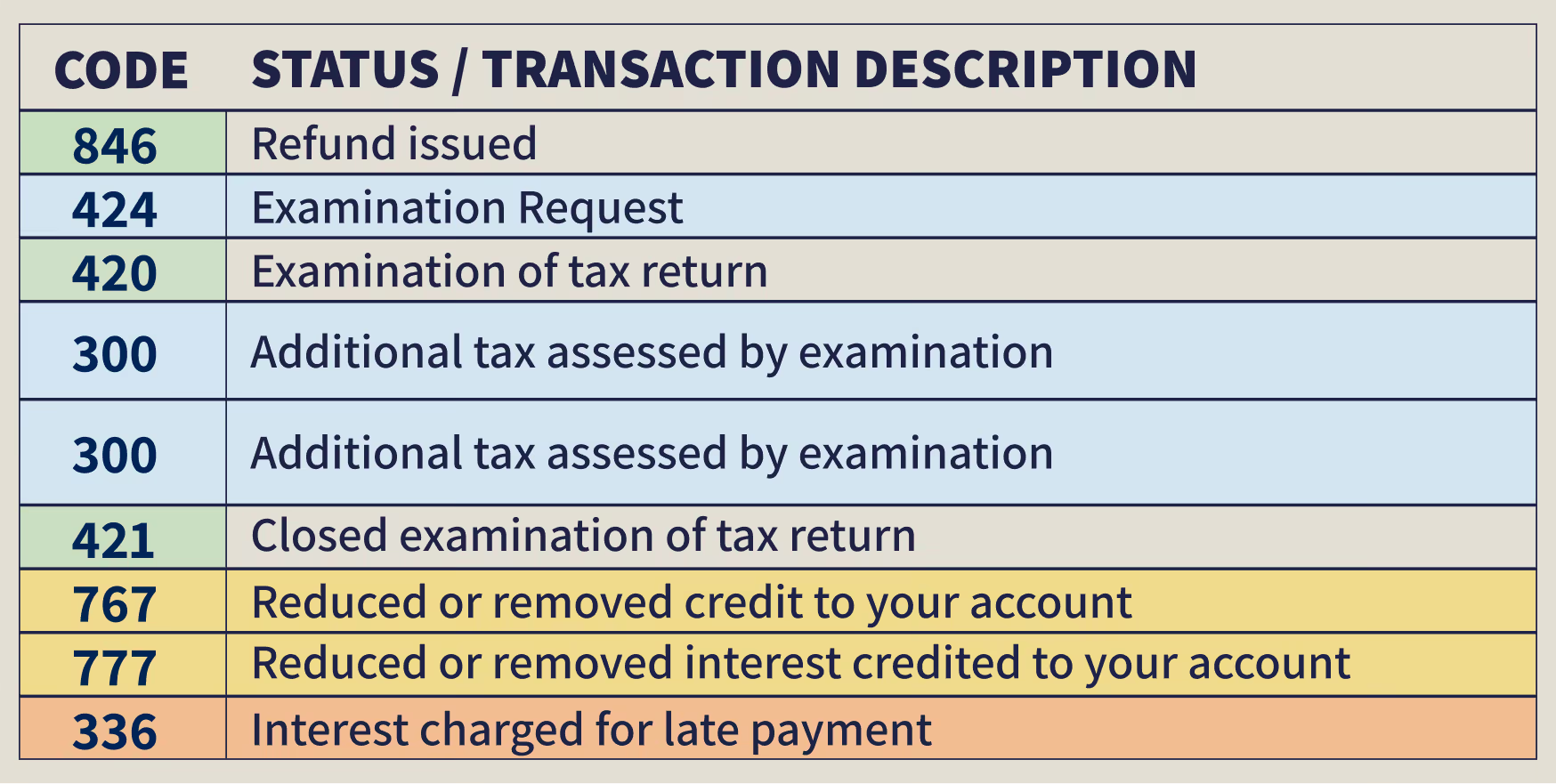

Businesses that repaid ERC assessments often see a similar sequence on their IRS account transcripts. After the IRS disallows the Credit, the transcript typically shows code 300, labeled “Additional tax assessed by examination,” followed by interest entries such as code 196 and code 336, both reflecting “Interest charged for late payment.” In these cases, the IRS begins calculating the underpayment interest starting on the date the ERC refund was originally issued (code 846, “Refund issued”). Because ERC refunds were often large, the resulting interest amounts can also be substantial.

The approach taken by the IRS assumed that the liability existed throughout the entire period between the refund and the later assessment. But the Kwong decision suggests that assumption may not be correct.

As discussed in an earlier article, If Kwong Is Right, the ERC Deadline May Be Wrong, co-authored with Zach Lyda, the Court of Federal Claims interpreted the 2019 version of section 7508A(d) as creating an automatic statutory postponement of certain federal tax deadlines during the COVID-19 disaster period. Under the court’s interpretation, the postponement period began on January 20, 2020, and continued until 60 days after the national emergency ended. Because the federal government declared the emergency over on May 11, 2023, the statutory postponement period extended through July 10, 2023, the first operative due date for affected tax acts.

Jessica Marine and Yan Wang discussed the broader implications of this interpretation, including how the disaster postponement may affect penalties and other additions to tax in their article, Kwong v. United States: Court of Federal Claims Holds COVID Disaster Declaration Mandated Suspension of Federal Tax Deadlines.

Interest on an underpayment generally begins to accrue when a tax liability becomes due and remains unpaid. If the statutory due dates relevant to ERC-related liabilities were postponed until July 10, 2023, then a fundamental question arises: Before that date, was there any tax legally due?

If the liability had not yet come due, there could be no underpayment. And if there was no underpayment, interest should not have accrued. Yet the IRS has frequently calculated interest beginning when the ERC refund was first issued—oftentimes months and years before July 2023. For businesses that repaid significant ERC refunds, the difference between those two timelines can translate into substantial amounts of interest.

This issue is most relevant for businesses that meet two conditions. First, they received ERC refunds before July 11, 2023. Second, the IRS later disallowed the Credit, assessed an amount as additional tax, and the taxpayer repaid the assessment along with interest. If the interest calculation includes periods before July 11, 2023, the taxpayer may have grounds to seek a refund of the amount paid from the IRS.

For many businesses, ERC disputes have already consumed significant time and resources. But for taxpayers who repaid ERC assessments and the accompanying interest, the story may not be finished. If the statutory postponement recognized in Kwong holds, some taxpayers may have paid interest for a period when the law treated the underlying liability as not yet due. For those businesses, the final chapter of the ERC saga may involve one more refund claim.

Taxpayers seeking to recover improperly charged interest must first pursue relief administratively. This generally involves filing Form 843, Claim for Refund and Request for Abatement, requesting a refund of the interest paid. If the IRS does not act on the claim within six months—or formally disallows it—the taxpayer may then pursue a refund suit in federal court.

The Frost Law team is available to help businesses evaluate whether they should pursue refunds of interest paid after an ERC refund is disallowed, as well as advising business on other continuing ERC clean-up issues including audits and examination, protests and appeals, alternative dispute resolution, including Post-Appeals Mediation (PAM), and refund claim lawsuit. Contact our team today at (410) 497-5947 or schedule a confidential consultation.

Over the past year, many businesses that received Employee Retention Credit refunds have completed the audit cycle. While many examinations have resulted in no change, in a growing number of cases, the IRS has disallowed the Credit and assessed some or all of the refunded amount as additional tax. Businesses then repaid the assessed tax, along with interest that the IRS calculated on the underpayment. For many of these taxpayers, repayment probably seemed like the end of the matter. But a recent court decision interpreting tax-related deadlines during Federally declared disasters may create an unexpected refund opportunity for many of those businesses.

If the Court of Federal Claims’ interpretation of section 7508A(d) in Kwong v. United States ultimately proves correct, some taxpayers may have paid interest that should never have accrued in the first place. To be sure, in matters currently being evaluated by our firm, interest overpayments routinely reach tens of thousands of dollars and in some cases climb to more than $50,000 or more. We encourage businesses that made repayment of ERC to review their situation to see if they might be in a similar situation.

Businesses that repaid ERC assessments often see a similar sequence on their IRS account transcripts. After the IRS disallows the Credit, the transcript typically shows code 300, labeled “Additional tax assessed by examination,” followed by interest entries such as code 196 and code 336, both reflecting “Interest charged for late payment.” In these cases, the IRS begins calculating the underpayment interest starting on the date the ERC refund was originally issued (code 846, “Refund issued”). Because ERC refunds were often large, the resulting interest amounts can also be substantial.

The approach taken by the IRS assumed that the liability existed throughout the entire period between the refund and the later assessment. But the Kwong decision suggests that assumption may not be correct.

As discussed in an earlier article, If Kwong Is Right, the ERC Deadline May Be Wrong, co-authored with Zach Lyda, the Court of Federal Claims interpreted the 2019 version of section 7508A(d) as creating an automatic statutory postponement of certain federal tax deadlines during the COVID-19 disaster period. Under the court’s interpretation, the postponement period began on January 20, 2020, and continued until 60 days after the national emergency ended. Because the federal government declared the emergency over on May 11, 2023, the statutory postponement period extended through July 10, 2023, the first operative due date for affected tax acts.

Jessica Marine and Yan Wang discussed the broader implications of this interpretation, including how the disaster postponement may affect penalties and other additions to tax in their article, Kwong v. United States: Court of Federal Claims Holds COVID Disaster Declaration Mandated Suspension of Federal Tax Deadlines.

Interest on an underpayment generally begins to accrue when a tax liability becomes due and remains unpaid. If the statutory due dates relevant to ERC-related liabilities were postponed until July 10, 2023, then a fundamental question arises: Before that date, was there any tax legally due?

If the liability had not yet come due, there could be no underpayment. And if there was no underpayment, interest should not have accrued. Yet the IRS has frequently calculated interest beginning when the ERC refund was first issued—oftentimes months and years before July 2023. For businesses that repaid significant ERC refunds, the difference between those two timelines can translate into substantial amounts of interest.

This issue is most relevant for businesses that meet two conditions. First, they received ERC refunds before July 11, 2023. Second, the IRS later disallowed the Credit, assessed an amount as additional tax, and the taxpayer repaid the assessment along with interest. If the interest calculation includes periods before July 11, 2023, the taxpayer may have grounds to seek a refund of the amount paid from the IRS.

For many businesses, ERC disputes have already consumed significant time and resources. But for taxpayers who repaid ERC assessments and the accompanying interest, the story may not be finished. If the statutory postponement recognized in Kwong holds, some taxpayers may have paid interest for a period when the law treated the underlying liability as not yet due. For those businesses, the final chapter of the ERC saga may involve one more refund claim.

Taxpayers seeking to recover improperly charged interest must first pursue relief administratively. This generally involves filing Form 843, Claim for Refund and Request for Abatement, requesting a refund of the interest paid. If the IRS does not act on the claim within six months—or formally disallows it—the taxpayer may then pursue a refund suit in federal court.

The Frost Law team is available to help businesses evaluate whether they should pursue refunds of interest paid after an ERC refund is disallowed, as well as advising business on other continuing ERC clean-up issues including audits and examination, protests and appeals, alternative dispute resolution, including Post-Appeals Mediation (PAM), and refund claim lawsuit. Contact our team today at (410) 497-5947 or schedule a confidential consultation.