If your business is not a partnership or S corporation, this may be the time to consider changing. If you are already a partnership or S corporation, we have good news!

The IRS is now allowing a workaround of the $10,000 limitation on the deduction by an individual of state income taxes for taxpayers in various states–including Maryland if certain requirements are met. Taking advantage of this new tax law means that your pass-through entity must take timely action.

The IRS issued a Notice this week indicating that it will allow deductions for state income taxes paid by pass-through business entities. The IRS treatment of these tax payments was previously uncertain, because such payments may allow small business owners to circumvent the $10,000 cap on itemized deductions. The IRS’s new stance, outlined in the Notice, is great news for Maryland business owners, because effective July 1, 2020 Maryland allows a pass-through business entity to elect to pay tax at the entity level for a Maryland resident owner’s distributive share of income

In order for a cash basis taxpayer to take advantage of this deduction, the entity must make an estimated payment to Maryland before year end. Then when filing the 2020 Form 510 there will be an election to voluntarily pay tax at the entity level. This will create a Federal deduction for the business entity–lowering the taxable income that flows through to the individual owner’s Federal income tax return. The amount of Maryland tax paid by the pass-through entity will then show up as a state tax credit on the Maryland K-1 which will offset personal state income tax.

For tax year 2020, the tax rates for this elective entity level tax are 8% for individual members of a pass-through entity and 8.25% for a corporate member. It is important to note that this can only be applied to income which is taxable to Maryland resident owners of the pass-through entity; the income of non-residents will remain subject to the normal Non-Resident Withholding rules (which is a distribution rather than a deductible tax). We will continue to monitor for any additional federal or state guidance and related developments pertaining to this workaround. The Maryland legislature is working on a technical corrections bill that may expand this treatment to non-residents retroactively. We advise you to consult a tax attorney before taking any steps.

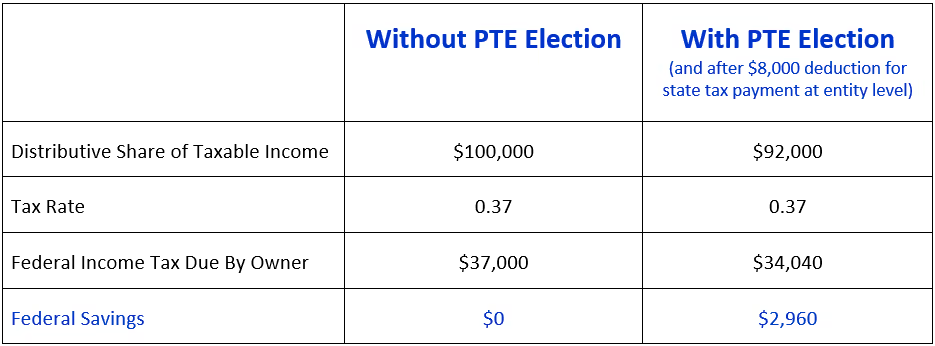

Below is an illustration of how this election can save the taxpayer Federal tax each year that the election is in effect. Note that there are special considerations that should be discussed when there are non-resident shareholders, and you should consult with your tax professional on necessary steps to take advantage of this opportunity while being fair to all of the owners.

Hypothetical example of Federal tax savings for an individual owner of a pass-through business entity:

Important note: You should consult with your tax advisor on how this applies to your specific circumstances.

Let us know if you need assistance with navigating these rules and/or calculating the amount of the estimated Maryland tax payment due. You can contact us at 410-862-2673 or fill out our brief contact form.

If your business is not a partnership or S corporation, this may be the time to consider changing. If you are already a partnership or S corporation, we have good news!

The IRS is now allowing a workaround of the $10,000 limitation on the deduction by an individual of state income taxes for taxpayers in various states–including Maryland if certain requirements are met. Taking advantage of this new tax law means that your pass-through entity must take timely action.

The IRS issued a Notice this week indicating that it will allow deductions for state income taxes paid by pass-through business entities. The IRS treatment of these tax payments was previously uncertain, because such payments may allow small business owners to circumvent the $10,000 cap on itemized deductions. The IRS’s new stance, outlined in the Notice, is great news for Maryland business owners, because effective July 1, 2020 Maryland allows a pass-through business entity to elect to pay tax at the entity level for a Maryland resident owner’s distributive share of income

In order for a cash basis taxpayer to take advantage of this deduction, the entity must make an estimated payment to Maryland before year end. Then when filing the 2020 Form 510 there will be an election to voluntarily pay tax at the entity level. This will create a Federal deduction for the business entity–lowering the taxable income that flows through to the individual owner’s Federal income tax return. The amount of Maryland tax paid by the pass-through entity will then show up as a state tax credit on the Maryland K-1 which will offset personal state income tax.

For tax year 2020, the tax rates for this elective entity level tax are 8% for individual members of a pass-through entity and 8.25% for a corporate member. It is important to note that this can only be applied to income which is taxable to Maryland resident owners of the pass-through entity; the income of non-residents will remain subject to the normal Non-Resident Withholding rules (which is a distribution rather than a deductible tax). We will continue to monitor for any additional federal or state guidance and related developments pertaining to this workaround. The Maryland legislature is working on a technical corrections bill that may expand this treatment to non-residents retroactively. We advise you to consult a tax attorney before taking any steps.

Below is an illustration of how this election can save the taxpayer Federal tax each year that the election is in effect. Note that there are special considerations that should be discussed when there are non-resident shareholders, and you should consult with your tax professional on necessary steps to take advantage of this opportunity while being fair to all of the owners.

Hypothetical example of Federal tax savings for an individual owner of a pass-through business entity:

Important note: You should consult with your tax advisor on how this applies to your specific circumstances.

Let us know if you need assistance with navigating these rules and/or calculating the amount of the estimated Maryland tax payment due. You can contact us at 410-862-2673 or fill out our brief contact form.