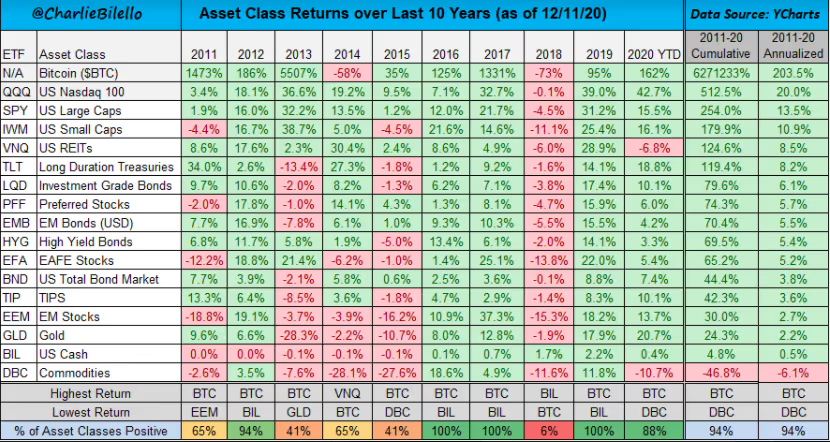

Today feels eerily similar to 2017. In December 2017, Bitcoin’s price hit $19,900; now in December 2020, after a three-year bear market, Bitcoin is at all-time highs trading above $20,000. The market is different now with the recent investments of large financial institutions, corporate treasuries, and hedge fund managers investing, whereas 2017 was shaped by the retail market (i.e., individual investors). It is clear many millionaires have been created in the cryptocurrency space over the last decade as it has been the top performing asset.

Amidst the meteoric rise of cryptocurrencies, tax guidance has not been the most robust. In 2014, the IRS issued Notice 2014-21, clarifying that cryptocurrency is treated as property for tax purposes. Although the IRS did not address IRC §1031 in that notice, many users believed that, as property, exchanges of differing types of cryptocurrency could qualify for IRC §1031 like-kind exchange deferral. However, this “loophole” was closed in 2017 in no uncertain terms. Pursuant to the Tax Cuts and Jobs Act, IRC §1031 like-kind exchange treatment is now specifically limited to real property. If you trade one crypto asset for another, you have a taxable gain or loss, much like stock gains and losses. Ironically, there are advantages to this treatment.

With long-term capital gains (held greater than one year), the tax rate for cryptocurrency, much like stock, is zero, 15% or 20%. One can strategically sell to take advantage of preferential rates. A client of mine is now worth millions in Bitcoin and has been able to retire early and live on his digital assets and traditional portfolio. As we work to balance out the overweighting in cryptocurrency and diversify into other income producing assets, we have strategically sold to minimize taxes.

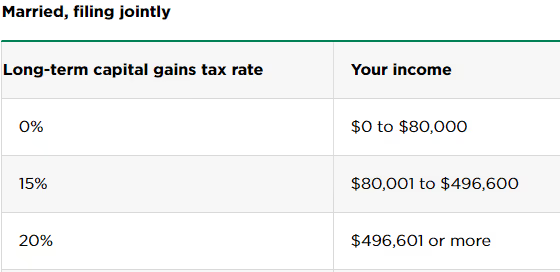

The first $80,000 of taxable income for a married couple is subject to a zero percent rate on long-term capital gains, assuming no other sources of income. The next roughly $400,000 of long-term capital gain is taxed at 15%. Let’s assume a family has $30,000 of qualified dividend income and $100,000 of long-term held cryptocurrency sales. The first $80,000 of $130,000 taxable income is taxed at zero percent and the remaining $50,000 is taxed at 15%. In this scenario, the taxpayer would pay $7,500 in federal income taxes (i.e., $50,000 x 15% = $7,500). Not a shabby tax bill on taxable income of $130,000. Provided income stays below roughly $500,000, all long-term capital gains are taxed at 15% or less.

From what I have seen, the developers and newly wealthy investors in the crypto asset boom have a more altruistic view on the world than other businessmen and investors. Some crypto asset developers try to bring banking to the forgotten third world, while some tokens are interested in preventing fraud and “going green”. Looking at the space as a whole, cryptocurrencies are trying to change the world for the better. With increasing IRS scrutiny, how can these new millionaires mitigate and defer tax dollars while diversifying their assets away from being so heavily weighted in one sector like crypto assets?

A taxpayer donates highly appreciated assets, in this case cryptocurrency, into a CRUT and then immediately sells the assets with the intent to create a diversified portfolio of income producing assets. The sale of the cryptocurrency by the CRUT does not cause an immediately taxable event to the trust or the non-charitable beneficiaries of the trust. The proceeds of the sale remain in the trust and may be reinvested in other assets. The trust distributes a fixed percentage of the value of its assets to a non-charitable beneficiary or beneficiaries of the taxpayer’s choosing. At the death of the last named non-charitable beneficiary, the remaining balance is distributed to the charity or charities identified in the trust. Provided the present value of the remainder interest going to the charity is greater than 10% of the contribution, the present value of the charitable remainder interest qualifies as a current tax deductible charitable donation.

Example: A 40-year-old taxpayer contributes $1,000,000 of Bitcoin to a trust and assigns a 7% payout rate with themselves as the income beneficiary. Using the IRS discount rates and tables, the present value of the remainder interest going to the charity at death would be roughly $101,000, satisfying the 10% test. Regardless of what the taxpayers’ basis, he or she gets a $101,000 current income tax deduction and also receives 7% of the fair market value of the trust distributed annually until death. For instance, if the market value of the trust is $1,000,000 in given year, then the distribution to the beneficiary is $70,000.

As the payout percentage decreases, the present value of the charitable donation would increase. For instance, a 5% payout percentage to the income beneficiary would yield a present value closer to $177,000

A summary of the benefits are as follows:

CLTs should not be overlooked. In a CLT, the income produced by the donated assets goes to a charity, but, after a specified period of time, the remainder goes to a beneficiary of the donor’s choosing. Given the current interest rate environment, a CLT may be perfect for those with other forms of wealth that can sustain a lifestyle while waiting for funds to be returned to their use.

Another option for highly appreciated assets is a Donor-Advised Find. This is a charitable giving vehicle that is administered by a public charity to manage donations. The donor surrenders ownership of the property (i.e., the asset), but retains advisory privileges over how the account is invested and distributed to charities. Please note that the donor has no income stream with this arrangement and should only be considered for those with the means and charitable intent this option necessitates.

Charitable vehicles offering lifetime income streams, current charitable tax deductions in excess of basis, and diversification of a portfolio heavily weighted in cryptocurrencies are extremely effective planning tools. Careful assessment of a taxpayer’s financial and charitable goals will determine the most suitable vehicle for that taxpayer’s needs.

Bestgate Wealth Advisors and Frost Law would always love to hear from you and offer a free consultation on financial planning, tax planning, or estate planning around digital assets. Between our registered investment advisory firm and full-service law firm, we can help.

You can reach Bestgate Wealth Advisors at 410-793-7479 and Frost Law at 410-862-2834.

Today feels eerily similar to 2017. In December 2017, Bitcoin’s price hit $19,900; now in December 2020, after a three-year bear market, Bitcoin is at all-time highs trading above $20,000. The market is different now with the recent investments of large financial institutions, corporate treasuries, and hedge fund managers investing, whereas 2017 was shaped by the retail market (i.e., individual investors). It is clear many millionaires have been created in the cryptocurrency space over the last decade as it has been the top performing asset.

Amidst the meteoric rise of cryptocurrencies, tax guidance has not been the most robust. In 2014, the IRS issued Notice 2014-21, clarifying that cryptocurrency is treated as property for tax purposes. Although the IRS did not address IRC §1031 in that notice, many users believed that, as property, exchanges of differing types of cryptocurrency could qualify for IRC §1031 like-kind exchange deferral. However, this “loophole” was closed in 2017 in no uncertain terms. Pursuant to the Tax Cuts and Jobs Act, IRC §1031 like-kind exchange treatment is now specifically limited to real property. If you trade one crypto asset for another, you have a taxable gain or loss, much like stock gains and losses. Ironically, there are advantages to this treatment.

With long-term capital gains (held greater than one year), the tax rate for cryptocurrency, much like stock, is zero, 15% or 20%. One can strategically sell to take advantage of preferential rates. A client of mine is now worth millions in Bitcoin and has been able to retire early and live on his digital assets and traditional portfolio. As we work to balance out the overweighting in cryptocurrency and diversify into other income producing assets, we have strategically sold to minimize taxes.

The first $80,000 of taxable income for a married couple is subject to a zero percent rate on long-term capital gains, assuming no other sources of income. The next roughly $400,000 of long-term capital gain is taxed at 15%. Let’s assume a family has $30,000 of qualified dividend income and $100,000 of long-term held cryptocurrency sales. The first $80,000 of $130,000 taxable income is taxed at zero percent and the remaining $50,000 is taxed at 15%. In this scenario, the taxpayer would pay $7,500 in federal income taxes (i.e., $50,000 x 15% = $7,500). Not a shabby tax bill on taxable income of $130,000. Provided income stays below roughly $500,000, all long-term capital gains are taxed at 15% or less.

From what I have seen, the developers and newly wealthy investors in the crypto asset boom have a more altruistic view on the world than other businessmen and investors. Some crypto asset developers try to bring banking to the forgotten third world, while some tokens are interested in preventing fraud and “going green”. Looking at the space as a whole, cryptocurrencies are trying to change the world for the better. With increasing IRS scrutiny, how can these new millionaires mitigate and defer tax dollars while diversifying their assets away from being so heavily weighted in one sector like crypto assets?

A taxpayer donates highly appreciated assets, in this case cryptocurrency, into a CRUT and then immediately sells the assets with the intent to create a diversified portfolio of income producing assets. The sale of the cryptocurrency by the CRUT does not cause an immediately taxable event to the trust or the non-charitable beneficiaries of the trust. The proceeds of the sale remain in the trust and may be reinvested in other assets. The trust distributes a fixed percentage of the value of its assets to a non-charitable beneficiary or beneficiaries of the taxpayer’s choosing. At the death of the last named non-charitable beneficiary, the remaining balance is distributed to the charity or charities identified in the trust. Provided the present value of the remainder interest going to the charity is greater than 10% of the contribution, the present value of the charitable remainder interest qualifies as a current tax deductible charitable donation.

Example: A 40-year-old taxpayer contributes $1,000,000 of Bitcoin to a trust and assigns a 7% payout rate with themselves as the income beneficiary. Using the IRS discount rates and tables, the present value of the remainder interest going to the charity at death would be roughly $101,000, satisfying the 10% test. Regardless of what the taxpayers’ basis, he or she gets a $101,000 current income tax deduction and also receives 7% of the fair market value of the trust distributed annually until death. For instance, if the market value of the trust is $1,000,000 in given year, then the distribution to the beneficiary is $70,000.

As the payout percentage decreases, the present value of the charitable donation would increase. For instance, a 5% payout percentage to the income beneficiary would yield a present value closer to $177,000

A summary of the benefits are as follows:

CLTs should not be overlooked. In a CLT, the income produced by the donated assets goes to a charity, but, after a specified period of time, the remainder goes to a beneficiary of the donor’s choosing. Given the current interest rate environment, a CLT may be perfect for those with other forms of wealth that can sustain a lifestyle while waiting for funds to be returned to their use.

Another option for highly appreciated assets is a Donor-Advised Find. This is a charitable giving vehicle that is administered by a public charity to manage donations. The donor surrenders ownership of the property (i.e., the asset), but retains advisory privileges over how the account is invested and distributed to charities. Please note that the donor has no income stream with this arrangement and should only be considered for those with the means and charitable intent this option necessitates.

Charitable vehicles offering lifetime income streams, current charitable tax deductions in excess of basis, and diversification of a portfolio heavily weighted in cryptocurrencies are extremely effective planning tools. Careful assessment of a taxpayer’s financial and charitable goals will determine the most suitable vehicle for that taxpayer’s needs.

Bestgate Wealth Advisors and Frost Law would always love to hear from you and offer a free consultation on financial planning, tax planning, or estate planning around digital assets. Between our registered investment advisory firm and full-service law firm, we can help.

You can reach Bestgate Wealth Advisors at 410-793-7479 and Frost Law at 410-862-2834.